By: Gene Williams, MAI, CCIM, Senior Appraiser & North American Data Center Valuation Director, Valbridge Property Advisors | Northern California

September 24, 2020

It’s all about POWER

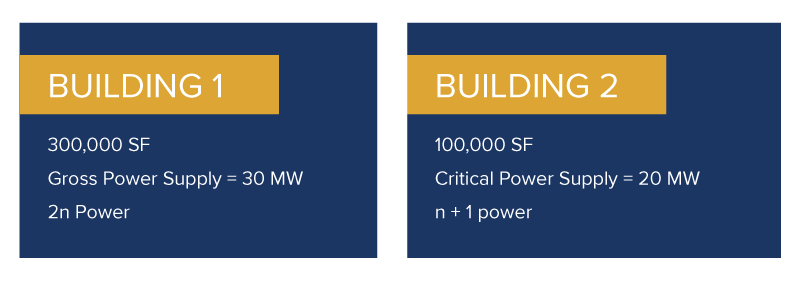

Critical Supply Vs. Gross Power (and redundancy)

Which one is likely to be more valuable? What if they have different PUEs (power utilization efficiency ratios) or power costs per kWh?

The power for Bldg. 1 is quoted as “Gross” whereas the power for Bldg. 2 is “Critical.” And while we do not know how the 2n power for Bldg. is configured, it is likely to only have about 15 MW of Critical power, indicating that Bldg. 2, with 20 MW of power, would be more valuable.

It is the Critical power supply that is the determining factor in determining data center values, not the size of the building. But what about PUEs and power costs, and what is “n + 1”? We’ll talk more about these issues later in the article. First, let’s define some basic terms.

“Raised Floors” and Other Terminology

Critical power is the “usable” or “sellable” power delivered to the Critical Computing Space, otherwise known as the Raised Floor Area. But since raised floors are no longer a necessary component – many operators are placing racks directly on the concrete floor with fiber, electrical and HVAC being provided from raceways in the ceiling, a better description of the space improved to host computers/servers is the “critical computing space.”

Power is measured by Watts as follows:

kW = kilowatts (1,000 watts)

MW = Megawatt (1,000 kW)

GW = Gigawatt (1,000 MW)

Power usage is measured in kWh, or kilowatt-hours, but that is for another article.

Since a data center is bought, sold and leased based on its Critical power supply, analysts rely on the $/MW or $/kW metric. Landlords and tenants negotiate leases based on the $/kW/Month paid to lease the Critical power supply.

By quoting rates on this basis, the power density is mostly removed from the equation as a valuation factor. So, a 20,000 SF critical computing area with 4 MW of power would produce the same gross income has 50,000 SF with 4 MW of power. But, at a power density of less than 100 watts/SF, the larger space would probably be more suitable to a telecommunications tenant that would not require high power density. Cloud computing, which is rapidly expanding under current conditions, requires power densities more like 200+ watts/SF.

Personal Property in a data center is NOT the electrical, cooling and redundant infrastructure. Imagine a high-rise office building without HVAC or electrical systems (or fiber optic lines). It wouldn’t be very valuable, right? Similarly, a “wholesale” data center is fully finished with these components, and would not be very valuable without them. Just like in an office building, these components are not considered personal property.

Personal property consists of the racks, servers and/or telecom equipment that is in the critical computing space. This is usually owned by the tenant. However, in a “colocation” facility, the landlord owns the racks, fiber optic lines and typically provides a variety of “managed services” that are “sold” to tenants on an a la carte basis. These facilities can reflect “business value.” Tenants are Customers in these facilities – they do not actually sign real estate leases – their contracts are called “licenses” and the landlord’s obligations are defined in the Service Level Agreement. As a result, a colocation facility is a fully integrated business, or “going concern” on a variety of levels.

Types of Data Centers

A Powered Shell is like a heavily improved warehouse. The landlord provides a hardened shell with the power stubbed to the building, and the tenant completes all the data center improvements. This is particularly common for tenants with high credit ratings (low costs of capital) like Amazon who would rather complete their own improvements in a building.

A Wholesale, or “Turnkey” facility includes all of the infrastructure necessary for a tenant to install their racks and servers. The Critical Computing spaces is leased in turnkey condition for the tenant to complete rack configuration and power/fiber distribution within the space. These “suites” or “pods” as they are sometimes called, are typically leased to tenants with power deployments of 250 kW or more (typically about 1 MW).

Colocation Facilities are designed to host servers for Customers who sign License agreements in order to place from one to dozens of servers in a facility. The “landlord” or Operator provides all of the infrastructure necessary for the Customer to install and manage their equipment. As previously mentioned, the Operator provides Managed Services to the Customer on an a la carte basis. These may include services such as Remote Hands, Software as a Service (“SaaS”), cross connects to other customers in the facility as well as a “Meet-Me-Room” where the Operator installs its own switching equipment to allow “Peering” between customers in the facility.

Again, colocation facilities are operating businesses. They are typically priced based on EBITDA multiples as well as cap rates.

Other types of facilities include Hyperscale, Edge and Carrier Hotels. Hyperscale facilities are usually leased by cloud services companies like Microsoft Azure or Amazon (“AWS”) as powered shells and then improved by the tenant. Recently, the typical size of these facilities has grown from about 30 MW to well over 100 MW per building.

Edge data centers are found at the “edge” of the network – often in the suburbs – these facilities bring “compute” to locations that are being under-served. Edge facilities stand to see exceptional growth as 5G, autonomous vehicles and other technologies like IoT put greater stress on networks.

Almost every major city has a Carrier Hotel. These facilities primarily operate as network hubs and switching locations that were originally constructed to support telegram and telephone networks. They tend to be high-rise buildings that have exceptional access to fiber optic networks. Usually located in central business districts, these facilities represent the “core” of network communications and routing.

Valuation Methods Overview

Just like other types of commercial real estate, underwriting is based on costs, sale comparables and income. However, data centers are analyzed on a $/MW (or $/kW) basis.

Construction costs can vary from $8 to about $13 million per MW, with renovation costs for older facilities being in the $3 to $5 million per MW range.

Sale comparables are analyzed based on location and physical factors. Currently, many sellers are “enterprise” or owner-users who built a facility for future expansion that was never needed. As companies move many of their applications to the cloud, they have become the largest sellers of previously-occupied facilities. Buyers of these properties want a significant discount to replacement cost, and most enterprise users have spent significantly more on their facilities than the market would typically bear. As a result, there continues to be a significant bid-ask spread in the market.

Other than REITs, the most active buyers are private equity firms and international government-sponsored entities. However, these firms usually partner with an operator to acquire a portfolio of properties, or the transaction represents a Merger & Acquisition deal. This limits transparency and makes valuation of individual facilities more difficult.

To establish income, an analysis of comparable lease transactions must be completed. Typically, parties involved in these transactions sign NDAs that limit their ability to share information. The data center market remains a very opaque business, as market participants hoard information. Under current conditions, many lease transactions are taking place without brokers, as the community of tenants and landlords remains relatively small.

Yield and cap rates tend to be higher in this segment, particularly for wholesale and colocation facilities. However, rates continue to fall for credit-leased projects with long remaining lease terms, particularly as the availability of capital in this segment continues to be very strong.

Valuation Issues

The following are the most significant issues that impact the valuation of data centers:

1. Location:

a. Power Costs

b. Access to fiber

c. Sales tax incentives

d. Free cooling

e. Exposure to natural disasters

2. Redundancy: 2n, n + 1

3. Power Efficiency: “PUE”

4. Power Density: watts per square foot

5. Ratio of Critical Computing space to total building area

What makes a good data center location? Cheap power, tax incentives and low latency with multiple fiber carriers. Northern Virginia is currently the most favored and fastest-growing location.

While Santa Clara in the Silicon Valley area continues to be a significant data center location, its costs are extremely high as compared to most other locations In this location, exposure to earthquake risk is mitigated by companies who have various locations. Most tenants want to avoid locations with flood risk or exposure to other natural disasters, including tornadoes and hurricanes. Generally, these locations are avoided, and locations with “free cooling” which is another term for cool outside air, are preferred. For instance, Toronto and Montreal, with very cheap hydro power and free cooling, represent two of the fastest-growing data center markets in North America.

Most facilities are configured for n + 1 redundancy, which means that the main power supply is backed-up by UPS systems and diesel generators. Most of these facilities reflect “Tier III” configurations. Tier I and II facilities are typically older and reflect much lower costs and values on a $/MW basis.

Power efficiency is simply a measurement of how efficiently a facility uses power. Since electricity is almost always paid by the tenant, a PUE rating is an important factor to a potential tenant.

With metrics based on power, the density of power in a facility has less of an impact on underwriting. However, high power-density Hyperscale facilities tend to reflect the lowest rental rates due to economies of scale in construction.

Finally, it is easy to understand that facilities with a low ratio of critical computing area to the total building area tend to sell at higher prices on a $/MW basis. Future expandability combined with other uses, such as disaster recovery space, tend to skew prices and create valuation issues.

Residual Value

What’s it going to be worth in 10 years when the infrastructure is dated? Will it still be a data center, or should it be valued as an industrial building or powered shell? These are common questions asked by equity investors and lenders. The answer is that a building with 5 MW of power today will still have 5 MW of power in 10 years.

The fact investors and market participants are projecting continued use of the facility as a data center at the end of the holding period is built into the capitalization rate. If capitalization rates were in the 15% to 20% range, then it would be clear that the market only values the relatively short-term income the facility can generate. However, capitalization rates are in the 6% to 9% range, indicating that a residual value based on the existing use is being projected by market participants.

However, to mitigate risk, underwriting is more commonly including annual reserves that are adequate to replace/repair electrical and HVAC infrastructure that are necessary to sustain the existing use.

Mounting a war chest of $3 to $5 million per MW in order to renovate infrastructure at the end of the holding period is the most reliable way to keep data center infrastructure consistent with the changing requirements of tenants. With annual reserves accumulating over the holding period, a lower discount rate would be reasonably supported. Mitigating risk is the lender’s/investor’s primary concern.

Recession-Resistant

Since the start of the COVID-19 pandemic, data center REITs have experienced increasing investor demand, reflecting increasing P/E ratios as most other types of commercial real estate have suffered with declining tenant demand and lower valuations.

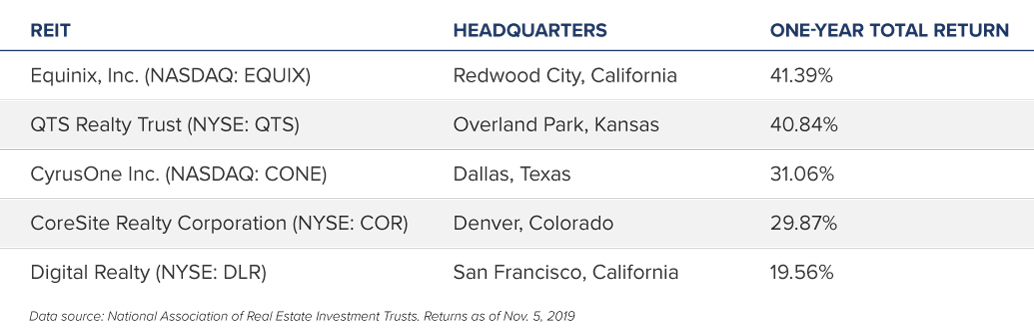

There are five data center REITs in the market today and they’re primarily based in the United States. These five have a total market cap of $89.5 billon and a 44.76% total year-to-date return as of Oct. 31, 2020, according to data from the National Association of Real Estate Investment Trusts. Data center REITs are enjoying a rebound in stock prices this year after big gains in 2016 and 2017 before falling off some in 2018.

Here is how the data center REITs rank in terms of return:

Long-term trends appear to be good for the sector. Milena Petrova, associate professor of finance at Syracuse University’s Whitman School of Management, said in an interview with U.S News earlier this year that data centers are a safer bet than investing in technology stocks. “The attractiveness of data REITs is in their high dividend yield, in contrast to most firms in the tech sector,” she said.

Analysts forecast that investors expect more digital connections to drive hybrid cloud computing and interconnectivity.

The forecast for data centers is positive thanks to a number of demand drivers that will likely keep data center REITs growing and expanding their operations.

Conclusion

Increasing demand for bandwidth and compute power has continued to drive strong fundamentals and an increasing supply of capital in this very specialized commercial real estate market segment. Work From Home and other changes in how business is done continue to drive data center demand.

While underwriting metrics are different from other types of real estate, and while market data and information continue to lack transparency, understanding and adjusting for the issues that impact valuations remains the most significant roadblock.

About the Author

Gene Williams, MAI, CCIM

Senior Appraiser & North American Data Center Valuation Director

Valbridge Property Advisors | Northern California

55 South Market Street, Suite 1210, San Jose, CA 95113

Office: 408.279.1520 x7150 | Cell: 408.772.9134

Gene Williams, MAI, CCIM, has over 30 years of experience in the commercial real estate industry as an appraiser, a loan broker and as a joint venture equity investor. Mr. Williams’ interest in data centers began in the early 2000s, and continued through his tenure at national brokerage firms, where he led data center valuation practices.

Mr. Williams has been a designated member (“MAI”) of the Appraisal Institute since 1994, is a Past President of the Northern California Chapter, and has authored a number of workshops and seminars that are approved for continuing education. Mr. Williams was awarded the CCIM designation in 1996.

Mr. Williams has provided expert witness testimony and arbitration services across the U.S., and is an active speaker/moderator and data center industry conferences. Mr. Williams has appraised all types of data centers, located in both the U.S. and Canada. These valuations have been performed for commercial banks, investment banks, private equity firms, data center operators and other investors.

The information contained in this publication is for informational and educational purposes only. It is not financial, legal, or other professional advice, and you may not rely on it for any purpose. To secure professional advice for your particular situation, you must engage one or more appropriate professional advisors to advise you about your situation.