By: Michele Wood, Director of Research, Valbridge Property Advisors | Houston

September 14, 2020

The word “hospitality” comes from the Latin hospes, meaning “host”, “guest”, or “stranger.” The Latin word ‘Hospital’ means a guest-chamber, guest’s lodging, or an inn. Hospes/hostis is thus the root for the English words host, hospitality, hospice, hostel and hotel. In 2020, just as hospitals are filling up, hotels have all but emptied out. How is the pandemic affecting hotel property values, and what can we expect in the sector over the coming months and years?

Impact on Values

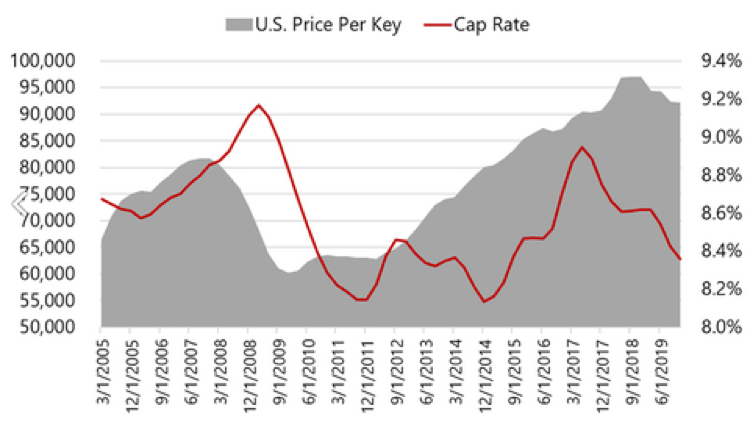

The number of transactions and the price for hotels are influenced by two primary factors: the availability of capital, and the performance of the sector as a whole. Toward the end of the Great Recession, hospitality performance bottomed out in late 2009. Well capitalized investors jumped in, and the number of transactions picked up in mid-2010. Mortgage capital became more available late in 2010, including on-book loans and CMBS lending.

2010 saw triple the number of transactions over 2009. There was a dip in 2012 caused by the debt crisis in the US and Europe, but it then picked up again in 2013 and stayed relatively steady through the end of 2019. According to Costar data, the number of hotel transactions in the second quarter of 2020 (which includes hotel, motel, and hotel casinos) was only 39% of the previous year’s transaction count: 886 transactions in Q2 2019 versus 342 in Q2 2020. The average price per room was less than half of what it was in 2019 for Q2.

Data shows a 5.5 year recovery from 2009 to 2015 for hotel asset pricing. This time frame may be a good metric for anticipating a post-COVID recovery, as global Air? passenger traffic is expected to be down until 2024.

HVS predicts the following impacts on hotel values:

- Sharp revenue declines will result in significant decreases in EBITDA, with the real possibility of negative EBITDA in the near term.

- The pullback of the debt market from the hotel sector, with lenders reporting lower loan-to-value ratios and/or higher spreads, will result in higher interest rates, despite the cuts by the Federal Reserve

- Capital market disruption may lead to all-cash transactions, seller financing, and other capital solutions that could put downward pressure on values.

Properties that are more vulnerable to negative value impact include full-service hotels dependent on group business (conventions and trade shows), gateway markets that rely on international travel, “fly to” markets such as Hawaii, airport markets, independent properties and markets that are influenced by the energy sector. Full-service hotels experience greater swings in revenue and EBITDA due to the high labor costs and other operating expenses.

By contrast, hotels that are likely to weather this storm better are hotels that are in “drive-to” markets, especially those with outdoor leisure draws such as mountains, lakes or beaches, suburban and small metro properties, extended-stay hotels, strong brand affiliates, and economy and midscale properties.

Although sector performance is critical to understand, the individual characteristics of each property are more important for valuation. The key factors are:

- Health of the local economy

- Demand generators

- Supply competition

- Tier, quality and condition of the property

- PIP requirements or capital improvements needed

- Historical financial performance

Richard Jander, Director of Hospitality Valuation for Valbridge in Houston and part of our National Specialty Practice Team, reports:

“Hotel Market trends can be summed up in two words, ‘it depends.’ The hotel market has not even begun to recover for some properties/markets while others never saw any changes at all. I appraised a couple of branded extended-stay hotels up in St. Louis that were running RevPARs above 2019 levels. I have also seen a select-service property that is dependent on corporate accounts of employees traveling to headquarters for training with maybe a dozen cars in the parking lots. It merely means that appraisers MUST fully understand the demand generators for a property and the market and how Covid-19 and/or oil prices have affected them.”

Cap Rates

Rates are derived from the trailing 12 EBITDA, which will differ in a downturn from the anticipated performance going forward. This will create a higher cap rate relative to a lower sale price. The cost of capital also will play a role in pricing as interest rates will rise and LTV’s will lower.

According to a recent HVS report, “During healthy economic periods, full-service hotel cap rates generally average 150 basis points below those of limited-service hotel cap rates. During the Great Recession, this differential decreased to 50 bps.”

Source: HVS: April 2020

Currently, we are seeing an uptick in performance in leisure drive-to markets, particularly those markets with outdoor generators. This may wane as the weather begins to turn and school gets fully underway. Economy and extended-stay properties are doing better than large full-service urban properties. April was a low point for performance, with occupancy rates around 20% on average. July was only up to 40%, where summer occupancy rates generally hover around 80%. For the week of August 9-15, rates climbed to 50.2%, according to STR.

What can hotel owners do?

The ability and capital to convert space into alternative uses may help some operators stay above water. Some may be able to convert to crisis use for quarantine, affordable housing for evicted tenants, or essential medical or nursing home staff housing. There are many risks associated with all these possibilities, including the risk of stigma attaching to a property used to house sick people.

One idea embraced by the Wythe Hotel in Brooklyn was converting rooms to office space in collaboration with co-working provider Industrious. Functioning in a similar way to the co-working model, but with the security and protection of a fully private office. This idea could catch on in more urban markets where many people have the need for office space outside of their homes, but cannot or do not want to return to their traditional offices.

Properties that are still open and serving guests are in a difficult position. Having to comply with ever—changing local regulations regarding closures and safety protocols, assuring potential and confirmed guests that the space is safe, and doing so with a much-reduced staff presents myriad challenges. For guests, the hotel experience is lessened by the situation and can create some disappointment when one cannot easily get towels refreshed or a hot breakfast or help with luggage.

The oldest hotel in the world is the Nishiyama Onsen Keiunkan in Japan. It opened in 705 A.D., more than 1,000 years before the American Revolution, and has been continuously operated since, owned by 52 generations of the same family. Hospitality may be in a crisis but it is not an existential crisis. In the United States, the oldest hotel is the Kelley House Hotel on Martha’s Vineyard, which opened its doors in 1742 as a respite for sailors. They have been open this summer to guests, while adjusting protocols to ensure safety. In response to a recent positive review on TripAdvisor, the General Manager wrote, “For 276 years people have been traveling to our historic property. The Kelley House has stood the test of time through wars, famines, pandemics, booms, and busts. We take our place in its history very seriously and we know the Kelley House will continue to welcome guests for generations to come.”

The information contained in this publication is for informational and educational purposes only. It is not financial, legal, or other professional advice, and you may not rely on it for any purpose. To secure professional advice for your particular situation, you must engage one or more appropriate professional advisors to advise you about your situation.