By Chris Singleton, MAI, CCIM

Senior Appraiser

In Part 1 of this series, we discussed how to value timber from pine plantation in the southeastern US using the Cost Approach. We talked about merchantable timber products and how the mix of those products can be likened to the mix of apartment units in a multi-family residential property. We also learned about premerchantable timber, and how its value is typically derived using some combination of the growth/cost forwarding method and discounting of future merchantable value. In Part 2, we will discuss the use of the Sales Comparison Approach (SCA) in timber appraisal, focusing on large, planted pine properties in the Southeastern United States.

As with the SCA in other properties, the goal for a timberland property is to estimate a reasonable value of the property as a whole by comparing individual components of the subject and comparables. And as with other properties, selecting the elements of comparison is the rub. Typical elements like zoning are often the same, while physical elements like frontage and flood zones are often so variable within properties, or inconsequential for the size and highest and best use, that they are either assumed to be similar between properties or considered irrelevant.

Property rights have traditionally always been fee simple, though over the last 5-10 years subsurface reservations have become more prominent and may occasionally require some small adjustment, but overall, this is minimal. Location in and of itself does not typically have much impact since investors care much more about the production potential of the property and the timber markets than they do about whether it’s in Mississippi or Alabama. So what do we compare?

Large industrial planted pine properties are all about land and timber, so land and timber are the primary comparisons. Although there are property-type nuances to land comparisons on timber properties, most commercial appraisers are already familiar with land valuation and adjustments, so as with Part 1 on the Cost Approach, we’ll focus only on timber here and leave land for another day. Simple, you say; we just adjust for the total timber value per acre between the subject and the comparable. To borrow a phrase from a college football icon, “Not so fast, my friend!” As we saw in Part 1 of this series on the Cost Approach, timber value has merchantable and premerchantable components, each of which needs to be analyzed separately. We’ll start with merchantable timber.

Merchantable Timber

If you will recall from the Cost Approach discussion, there are five basic “buckets” of merchantable timber value in a southern pine plantation: pine sawtimber; pine chip-n-saw; pine pulpwood; hardwood sawtimber; and hardwood pulpwood. Each of these must be considered when comparing two properties from the standpoint of both the difference in physical quantity and mix of the products as well as the difference in markets between the properties. The result yields two separate adjustments: a merchantable mix adjustment and a timber market adjustment.

Mix Adjustment

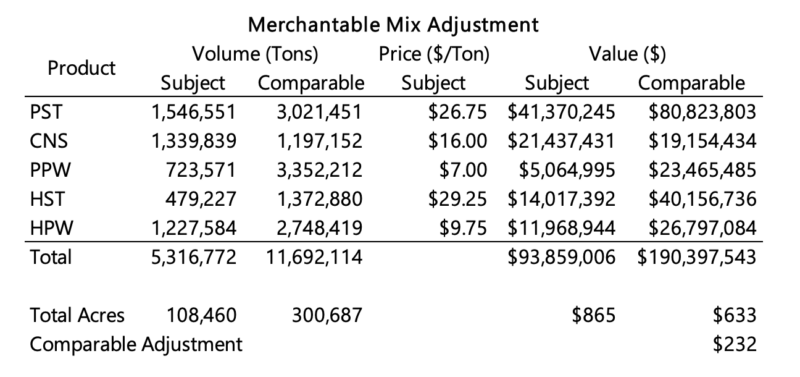

The merchantable mix adjustment is designed to isolate and adjust for the difference in quantity and product mix of merchantable timber. In a nutshell, it is the per acre difference between the subject at subject pricing and the comparable at subject pricing. The table below provides a real-world example from the appraisal of a large, planted pine property in Texas.

The timber prices for the subject property that were developed in the Cost Approach were applied to each of the five product volumes for both the subject and the comparable sale, with the resulting total values divided by the total acreage for each. The resulting $633/acre value for the comparable sale was then subtracted from the $865/acre value for the subject to yield the derived $232/acre merchantable mix upward adjustment to be applied to the comparable sale. The significant upward adjustment is because the subject has a timber product mix skewed more toward higher value products.

Timber Market Adjustment

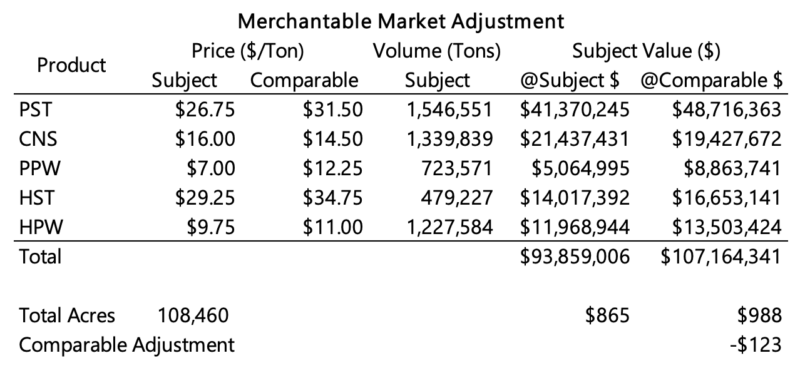

Where the mix adjustment is designed to adjust for the difference in timber product volume between the subject and the comparable, the market adjustment is designed to account for the difference in timber pricing between the subject and the comparable. This market adjustment accounts for both the difference in the relative strengths of the subject and comparable wood buckets (think location) as well as the difference in overall market conditions between the appraisal effective date and the comparable sale date (think time.) This can be thought of as the mix adjustment in reverse, holding the volume steady and applying both the current subject pricing and the comparable pricing at the time of sale to the subject volume. The table below shows this calculation using subject and comparable information from the same appraisal in Texas.

The timber prices for the subject property and for the comparable were applied to the product volumes for the subject, with the resulting total values divided by the total subject acreage. The resulting $988/acre value for the comparable pricing was then subtracted from the $865/acre value for the subject pricing to yield the derived $123/acre downward timber market adjustment to be applied to the comparable sale. The downward adjustment is because the comparable prices are stronger across the board than the current prices for the subject property.

The sum of the two merchantable timber adjustments is $109 and can be presented as the two separate mix and market adjustments or, if a “cleaner” grid is preferred, as one merchantable timber adjustment.

At this point, if you’re like me, you’ve calculated the unadjusted subject and comparable per acre timber values, subtracted them, and realized that there is only a $14 per subject acre difference between that and the combined mix and market adjustments calculated above. And, if you’re like me, you’re asking, “Why go through all that if there’s only a $14/acre difference?” It’s a fair point. But that $14/acre, when applied to the subject’s 108,460 acres, amounts to an additional $1.5 million in value; not huge on a percentage basis but not peanuts either. But the more important reason is that this level of analysis is what our peers (experienced timberland appraisers) do and it is what institutional investors and clients expect on properties like this.

Premerchantable Timber

Now that we’ve addressed adjustments for merchantable timber, we can move to premerchantable timber, which is similar, though slightly less straightforward. Premerchantable timber also has mix and market adjustments, and the mechanics are the same as for merchantable timber. However, because premerchantable timber values incorporate a growth component as part of the calculation, the premerchantable market adjustment also captures an element of property productivity. Each age class may be compared individually, or they may be grouped into multi-age strata at the appraiser’s discretion , though this decision is often dictated by the data available in the comparables sales. Regardless of how it is done, it is important to maintain a consistent process of comparison across all comparables.

Premerchantable Mix Adjustment

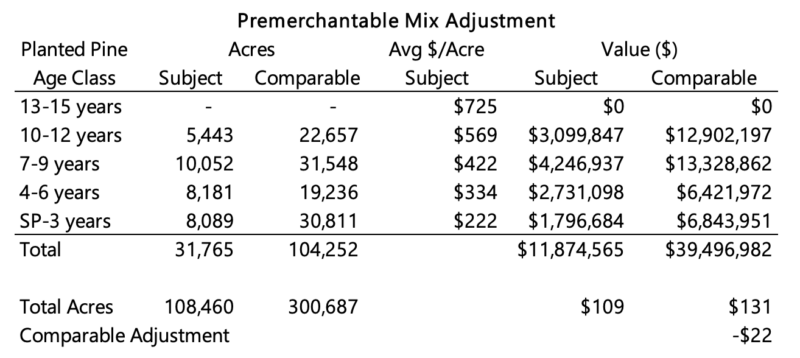

While the merchantable mix adjustment is designed to isolate and adjust for the difference in product mix, the premerchantable mix adjustment is designed to isolate and adjust for the difference in premerchantable planted pine age classes. Like the merchantable mix, it is the per acre difference between the subject at subject pricing and the comparable at subject pricing. The table below provides an example of a premerchantable mix adjustment from the same appraisal of a large, planted pine property in Texas.

In the table above, premerchantable acreage has been grouped into five separate strata. Recall that Part 1 of this series on the Cost Approach noted that age 15 is often considered the age of merchantability in southern pine plantations. However, this is highly variable, depending on the market and productivity of an individual property. The age 13-15 strata has been included even though it does not have any acres in order to illustrate that the age of merchantability for these two example properties is age 12, meaning that the age 13-15 strata has no acres. There may be other comparables that have a merchantable age higher than 12 and, therefore, will have acres in the age 13-15 strata.

Regardless, the important point to remember is that the subject and each comparable must be compared in the same way using the same process. In other words, each of the comparables must be analyzed with the same age classes or strata classes and then compared to the subject in the same manner. You cannot use seven strata for one comparable and five for another; they all need to be consistent so the comparisons to the subject are consistent. This includes treating each comparable with a consistent age of merchantability.

The strata average of the premerchantable per acre values for the subject property that were developed in the Cost Approach were applied to each of the five strata for both the subject and the comparable sale, with the resulting total values divided by the total property acreage for each. The resulting $131/acre value for the comparable sale was then subtracted from the $109/acre value for the subject to yield the derived -$22/acre premerchantable mix upward adjustment for the comparable sale. This relatively small adjustment indicates that the percentage of premerchantable acreage, and the mix of those acres, is relatively similar for the subject and the comparable.

Premerchantable Market Adjustment

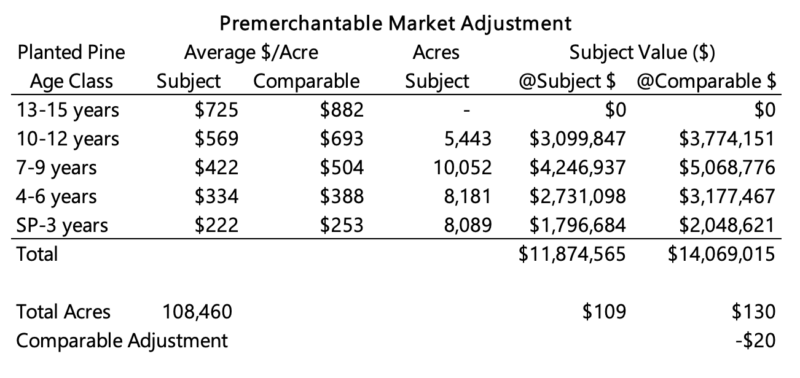

As with the merchantable market adjustment, the premerchantable market adjustment is designed to account for the difference in timber pricing, or in this case, premerchantable value per acre, between the subject and the comparable. The table below shows this calculation using subject and comparable information from the same appraisal in Texas.

The average values per are for each strata for the subject property and for the comparable were applied to the total acres in each strata for the subject, with the resulting total values divided by the total subject acreage. The resulting $130/acre value for the comparable was then subtracted from the $109/acre value for the subject to yield the derived $20/acre downward premerchantable market adjustment. As with the premerchantable mix adjustment, the relatively small adjustment indicates that the subject and comparable are relatively similar.

Conclusion

Making timber adjustments in appraisals of industrial timberland is more complex than simply comparing the overall per acre timber value of the subject to the comparable. It is important to analyze both the mix and the market for both merchantable and premerchantable timber in order to achieve the level of analysis expected by clients, competitors, and other market participants. These adjustments, when applied along with more familiar transactional and physical property adjustments, can help appraisers produce a detailed and reliable Sales Comparison Approach value estimate for a timberland property.

Now that you know how to develop the Sales Comparison and Cost Approaches on industrial timberland properties and are two-thirds of the way to being a timberland valuation expert, we will complete your training in the next installment on the Income Approach.

[1] It is here that I will point out that in order to develop the following adjustments, one must have sufficient detail on both the subject and the comparable sales in order to do so. This information is typically available for large, investment-grade timber properties but is often not available for small properties and properties that have not been professionally managed; for these properties, a total timber per acre adjustment, often based entirely on an appraiser’s or forester’s visual estimate, may be the only option.

[2] Because there may be as few as 10 up to 20 or more age classes (inclusive of age 0 stands that were just planted and site-prepared but not yet planted stands) it is common to group these into multi-age strata rather than treat each individual age class separately.

[3] This may mean adjusting the merchantable volume used for the merchantable timber adjustments in order to avoid double counting. For example, if a comparable is in a market where the merchantable age is 12, but your subject merchantable age is 15, then in order to include the comparable’s age 13-14 acres in the premerchantable adjustments, any volume in those age 13-14 acres cannot be included in the merchantable timber adjustments. Confused yet???

The information contained in this publication is for informational and educational purposes only. It is not financial, legal, or other professional advice, and you may not rely on it for any purpose. To secure professional advice for your particular situation, you must engage one or more appropriate professional advisors to advise you about your situation.

Related Services

Comprehensive Valuation & Advisory Services